One of the most difficult decisions you make in your life is whether to buy a house or keep renting. You will hear over and over that when you rent you’re throwing money away and when you buy a house that means you’ve hit the American dream!

I want to say this about renting, renting is not throwing your money away. You need a place to live and there’s someone out there that has taken a risk to buy a building and let you live in it.

So, it’s a difficult decision for them to decide “Who am I going to rent my house or apartment to, where do I draw the line?”

So while you might be thinking “Oh! Renting is throwing money down the drain”, the person whose spent their live savings on an investment of an apartment building or rental house, is actually placing their trust in you.

And now let me say one other thing. If you didn’t buy your house for cash you don’t own your home, the bank owns your home, the lender owns your home. You have all the responsibilities of the property tax, insurance, repairs and maintenance hot water heaters, a garage is flooding, sewer system problems, electrical problems.

But the bank actually owns your home and don’t for a minute think they wouldn’t take it back if you screw up. So, renting is a smart thing to do until you’re perfectly capable of handling all the extra responsibility of owning your own home.

So, if we bust the rent myth we might be a lot happier in our life and not be envious of those who own a home. Yes, what you’re doing when you rent is your paying someone else’s mortgage but you’re also, having the privilege of living in a space that doesn’t belong to you and is not your responsibility.

Today we will cover the dreaded discomfort zone known as insurance. People who want insurance and can’t get it, and people who have it can’t use it… so then why do we need it?

We need insurance for insurance…

Let’s take medical insurance as an example:

It’s actually against the law right now not to have medical insurance, and you can get fined for it. Or lets look at auto insurance.

Auto insurance is a must. If you’re stopped by a policeman and cannot produce auto insurance, you’re in trouble. There are others that are not mandatory but are probably a good idea to invest in….

One underused insurance that’s probably needed is renters insurance. It covers you for the things you own. So, let’s say you have a brand new sofa, stereo equipment, a 52” screen TV, and a refrigerator. You put a value on those things and you call up your insurance company.

Another one that’s important is life insurance. We do this so that when we die, somebody we love might get some money or others like a credit card company or a debtor will get paid off from your life insurance. And I believe it’s good to get life insurance at a very young age, I think you should always think ahead.

There’s Whole Life and there’s Term Policies. Term Policies are normally cheaper while Whole Life gives you something like a savings account. Also in the insurance industry they have something called Long Term Health, those of us who are 65 and older know what that means.

That means that if you fall down and you need to be in a care facility for a couple of months you have insurance to pay for a part of that.

There’s also minimums and maximums and there’s all kinds of rules on them… I got my long term health care policy in my 40s and my premium has been pretty low because of that.

So, if you’re in your 40s and 50s and you’re listening to me, look into long term health.

Now, you must be wondering: do all these insurances cost a lot of money? Yes they do and sometimes you can be “insurance poor”. That basically means you’re paying so much in premiums but you don’t really have the money to do so.

What I would like to do going forward is to go more in depth on each of these insurances for you to learn how to prioritize which ones are the most important ones for you…

How much does bad credit cost you? We discuss the importance of your credit report and what type of transactions affect yours.

Allow me to talk about consumer debt and maintaining good credit.

Here are some of the factors that show up on your credit report: your mortgage, credit cards, student loans, debt, medical bills and many more.

We tend to talk about credit reports like it’s a grown up thing, but actually, once you get a social security number and you do anything like going to a mall and opening up a $300 credit card at Pacific Sun Wear for example, that instantly goes on your credit report even as an 18 year old.

And notoriously, 18 to 25 year olds destroy their credit before they even really know what their credit score is or before they ever need their credit for something like an apartment or a car lease.

It’s important for you to know how much bad credit can cost you.

For example:

If you have bad credit and you put your name on a utility bill for your first apartment, the utility company might charge a whopping deposit. Now, they might charge you for that upfront or in installments as you pay every month.

There’s a push right now to get people who pay their rent on time to be able to use that Renter’s Credit as part of their credit score. So, whereas someone who is paying a mortgage is getting a boost to their credit score for paying their mortgage on time, there will be a boost to your credit score for paying your rent on time.

The other thing you can do to build your credit if you have bad credit is to apply for some pre-paid cards. These are cards that you put money in so you can then use them as a debit or credit card.

A prepaid credit card can build your credit and give you the opportunity to get a non-pre-paid card after a year or two.

One thing to keep in mind is thatbanks and the creditors like to see available balances high and the balance due very low… that’s how they determine your credit scores if you’re going to get credit from them… So if all your credit cards are maxed out you’re probably in trouble because they’re going to see that you don’t have any credit available to you and you might be opening another credit card because you’re desperate.

One other thing that might start to affect your credit report is your presence on social media. If a creditor thinks that your behavior is risky, they might be more inclined to turn you down for credit.

All those things are part of your credit picture now due to the internet and easy access to information. Your credit score is made up of a lot more things than it used to be when I was young…

The problem with credit card debt is not that we use credit cards, it’s that we don’t understand credit cards. Credit cards are unsecured credit…

This means that if the bank gives you a credit card there’s nothing they can come after if you don’t pay up. When you get a mortgage on a home they say “okay you didn’t pay your mortgage so we’re taking your home back” or if you have an auto loan and you don’t make your payment they come and take your auto back.

So, what does the bank do to feel better about the fact that they’ve given you unsecured credit? First, they give you an interest rate which can range from a 0% introductory rate all the way up to usually 14% or 15%.

Whatever your credit score is, that is going to determine your interest rate.

Secondly, don’t be late with your credit card payments, if you absolutely must, have the auto debit come out always on the due date, so that you’re always on time. And then during the course of the month pay it down even more.

You pay the minimum payment by auto debit and then you go ahead mid-month and make a bigger payment so you will pay down your credit card faster.

Thirdly, if you have a credit card that’s paid in full please don’t close it… keep that credit card open and put it away. Your credit score looks at how much credit is available to you and how much you have used.

It’s also very important to keep in mind that promo interest rates last a very short time. You might know these as introductory rates. What this basically means is this: we’re going to get you into our web with this incredible rate. However the little fine print says you might get screwed over and end up at 28.99% if you make one mistake, so it’s very important you don’t make mistakes.

It’s also important you educate yourself on compounding interests.

So make sure you read the fine print and understand the deals that you are signing with your creditor.

Okay, today we are going to discuss borrowing money from a friend or a family member.

I’m going to say it’s a bad idea, if you say you’re going to borrow money that means you’re going to pay it back. It creates a very awkward situation with friends and family when you borrow money.

But if you do have to borrow money in case of an emergency, come to them with the solution not the problem. Come to them and say “I need to borrow $4000, and this is what I’m going to use it for. If you allow me to borrow the money, this is how I will pay it back” and then stick to that no matter what. Remember, lives and relationships have been ruined by family members and friends who borrow money.

Normally, if you borrow money from an institution of any kind, you would be paying interest.

So, it’s only fair if you decide and I’m saying IF you decide to borrow money from a family member, a friend or a coworker that you pay them an interest rate that is slightly higher than the lowest interest rates.

In other words if the current interest rate is 3.5% pay them 4% because they’re actually giving you money from their pocket counting on you to return it.

You should never owe someone $15,000 for 10 years.

I will tell you there are some scary things about borrowing money from friends and family. Let me give you an instance, you borrow $4,000 from somebody so you can buy an updated computer because you don’t have room on your credit card and you don’t have cash.

So, you go to a friend that you know has cash put aside and you say, “I need to buy this computer for my work , Ipromise I will pay it back. I will give you 4% interest and I will give you $400 a month for the next 10 months.” Your friend is a little uncomfortable, your friend is a little squirmy but says “you know I believe in you, we’re good friends, here is the money.”

Then 2 months later, you have not paid them any money back and you’re on vacation or you buy a car or you’re out spending money at clubs or doing something like that. The only way it is safe to borrow money from a family member, a friend or a coworker is that you have the payback set out in paper, you sign a note and you agree to this and under no circumstances do you break that agreement.

That means if something comes up for you to go to on a ski trip and you owe someone $800 you say to your friends “I’m sorry I can’t go on that ski trip. I owe my friend who got me out of a jam money .”

That’s the way to be honorable, that’s what we do when we have integrity and dignity: we honor our word.

As children we had things in our lives that scare us, things that make us happy, different smells that bring up emotions in us, different people in our lives, and different experiences.

What we don’t understand is those things go with us to our adulthood and one of the most prominent is money. Think about it: What was your relationship with money when you were a child?

I know what mine was.

When we were kids we were not allowed to talk about money, we were very poor and my dad came in and out of our lives. When my mother and father did speak about money they were usually screaming at each other, they either screamed at each other or nobody spoke. So, in our household the subject of money was very tense, very scary. I didn’t understand how money worked when I was 4 or 5 years old. Yet I knew we didn’t have any and I knew that having money made things better and not having money made things worse.

So, as I got older and I started babysitting, I would hide my money away. There would be things that I could have bought with it yet I chose not to because I was afraid to lose $5. Back then when you babysat you made 50 cents an hour if you were lucky.

So, I started feeling very anxious about my money and sticking it in my underwear drawer or my sock drawer. It wasn’t until I got into high school that I started putting it in a little savings account because my mother worked at a bank. So, when I was in high school I started really understanding how it much cost for my mom to have me in her life… my uniforms, my books, anything we needed, food, gasoline, groceries. We knew when we were low on money because we had waffles or pancakes and scrambled eggs for dinner because we didn’t have money for meat or vegetables.

So, I started to develop this relationship of anxiety with money and if you look back to your childhood, you can see that the relationship you have with money now is a relationship that started a long time ago…

It’s very important to look at that relationship now when you have money. Are you anxious? Are you having struggles with buying something you want and feeling guilt from it?

Our relationship with money from our childhood is one of the most important things you’re going to learn when we start going forward.

Parents feel like they can’t speak to their children about money yet we need to talk to our children about money and how it works. You don’t need to scare them, you don’t need to give them anxiety about it but you do need to speak to them about how money works in your household.

So, let’s say you and your husband are working and the money comes in to the house. Well you have to think of your household like a team and your children need to be part of the team. They need to know that yeah, maybe the kid down the street is getting a car for his birthday or he just got abike or he is going to take ice skating lessons, but we can’t and here’s why.

If you tell children why, if you speak to your spouse or your significant other with whom you’re sharing expenses about the why and the what you will not argue and feel as anxious. Start talking about it to your children and with your spouse. There should be no secrets… it shouldn’t be about “oh! I just spent $35,000 on a purse, I can’t tell my husband that.”

Think back to your first job or think about the first job you’re going to take. You may be a mom entering the work force at the age of 40, you may be a college student, or you might even be a high school student who is about to get their first job at the local business in your area.

I’m going to tell you about my first job experience at 17 and see if you don’t feel the same way. I had just finished high school and I had borrowed money to get through my senior year of high school for tuition, actually my mother borrowed the money from a coworker.

I needed to go to work to pay that back. So I found a job at a pharmaceutical company in Los Angeles; I was hired as the inventory controller.

So, they gave me paperwork to fill out that you would know as a W-4. The W-4 states if I am single, married, single with children, single with no one, married with just a spouse, or married with children. And it asks you for that because the government has a rather complicated formula to figure out how much tax will be deducted from your check.

I really didn’t understand that tax would be deducted from my check. I was hired at $300 per month. Which meant that I would get 2 checks a month of $150 gross(remember the term gross, because the difference between gross and net is where all those taxes are).

I think my net check ended being $119. I went in to the controller and said I don’t understand what is Social Security and Medicare and I don’t understand who decided how much Federal and State tax would come out. So, he sat and explained it to me that social security was X % amount , Medicare was X % amount and those had to be paid. As for Federal and State there’s a really big formula and a very thick book that determines that.

So, he went over all of it with me which was really nice, and then I said “okay I guess what I have to do is just live on what the net is, not the $150 paycheck. I actually worked there 2 years, and right after Christmas in the New Year I received what was called a W-2.

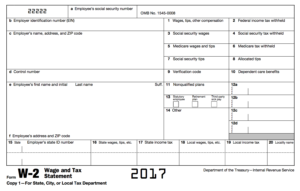

A W-2 is reported to the government about what you made in your paying job, remember that if you’re called an employee you will get a W-2. Now I don’t know how many of you, don’t open your W-2s but it’s really important that number 1 you look at your pay stabs every time you get them and at the end of the year you check out your W-2.

What your W-2 tell you is your gross wages, what your wages were before you got taxed, and then it will give you how much Federal tax you paid, how much social security you paid, how much Medicare you paid in and believe me if you’re like me I’ve been paying into those systems since I was 17 years.

So, there’s no way those are entitlements for me. Those are literally things that I’ve paid into for 48 years . So, I’m entitled to those things but those are not entitlements.

So, let’s go to the W-2 and it says these are your gross wages this is what you made before we took out the tax and now they have a box for Federal taxes and then they have a box for social security wages and Medicare wages.

If you live in a state like I do California where you get State tax it will also show you at the bottom how much state tax you paid and if you paid in to any disability programs if you have a 401K or a retirement plan, your W-2 is the thing that gives you the snap shot of your entire year.

Now, normally you get a W-2 at the end of January after the year closes, but if you quit your job in the middle of the year you would be allowed to ask for an interim W-2.

You might be one of the countless men and women who think overdraft protection is a good thing…

I’ll show you why you’ve been led to believe that and what the truth behind it really is.

Let me start off by saying that there might be rare instances where overdraft protection might help you. For example, if your rent check would bounce or your mortgage payment wouldn’t go through …

Yet in reality, here’s what overdraft protection really is: it’s a loan from the bank to cover mistakes that you might make in math.

You should never be relieved to use overdraft protection. Overdraft protection is something that you should ideally never touch…

It is a loan and it costs you money. Overdraft protection has to be paid back, the bank might either take the money back automatically next you time you deposit, or you might have to make a separate payment… it depends on your specific bank

and contract.

And keep in mind, since the bank sees you as a financial risk, there might be substantial interest applied to this loan.

You cannot rely on overdraft protection just as you can’t rely on your credit card to cover you when you don’t have money in your checking account.

I’ve even heard that some banks are talking about getting overdraft protection on your credit score. Can you imagine? It’s really not a good thing to have your credit score go down because of an overdraft protection mistake.

Now, I don’t know if any of you heard of this amazing story…

There was this female university student from London. The bank apparently made a mistake and gave her overdraft protection for everything she was buying. And even though she had virtually nothing in her checking account, she managed to spend around $3 million in overdraft protection.

And guess what? The bank considers it a loan and she has to pay it back.

So here you have this young college student who thought “Oh! I’m not even getting what’s going on but the money is always there in my account!” To be honest, I’m not quite sure what she thought.

And this is a prime example of you not keeping track of your funds… No one should really want or need overdraft protection. Just remind yourself: it’s not a good idea, its not a good idea.

It should be there only in case of an emergency situation, and hopefully if you’ve been going through our videos, you’ll be prepared to avoid those situations altogether.

It’s important to learn to live within our budget (except for emergencies which everybody has). We also want to learn to have discretionary funds which means we have money to play with. This is what you want to do instead of using overdraft protection.

Because all that will cause you is anxiety, sleepless nights, guilt, anger, and even shame. So let’s do things the right and healthy way and say no to overdraft protection.